What Is Credit?

The Complete Guide to How Credit Works

The Definition of Credit

Credit is your financial reputation—a measure of how reliably you borrow and repay money. It consists of three key components:

1. Credit Reports– Your financial report cards (maintained by Equifax, Experian, and TransUnion)

2. Credit Scores– A 3-digit number (300-850) predicting your repayment risk

3. Credit History– A record of every loan, credit card, and payment for the past 7-10 years

Key Insight: 90% of lenders use FICO Scores, which weigh:

> Payment history (35%)

> Amounts owed (30%)

> Credit age (15%)

> New credit (10%)

> Credit mix (10%)

How Credit REALLY Works (Behind the Scenes)

The Credit Bureau Process

Credit bureaus collect data through a system called Metro 2® where:

Lenders submit monthly updates about your accounts

The system automatically flags late payments after30 days delinquent

Errors often occur when data is transferred between institutions

Shocking Fact: A 2023 Consumer Financial Protection Bureau (CFPB) study found1 in 5 consumers had errors on their reports that could lower scores.

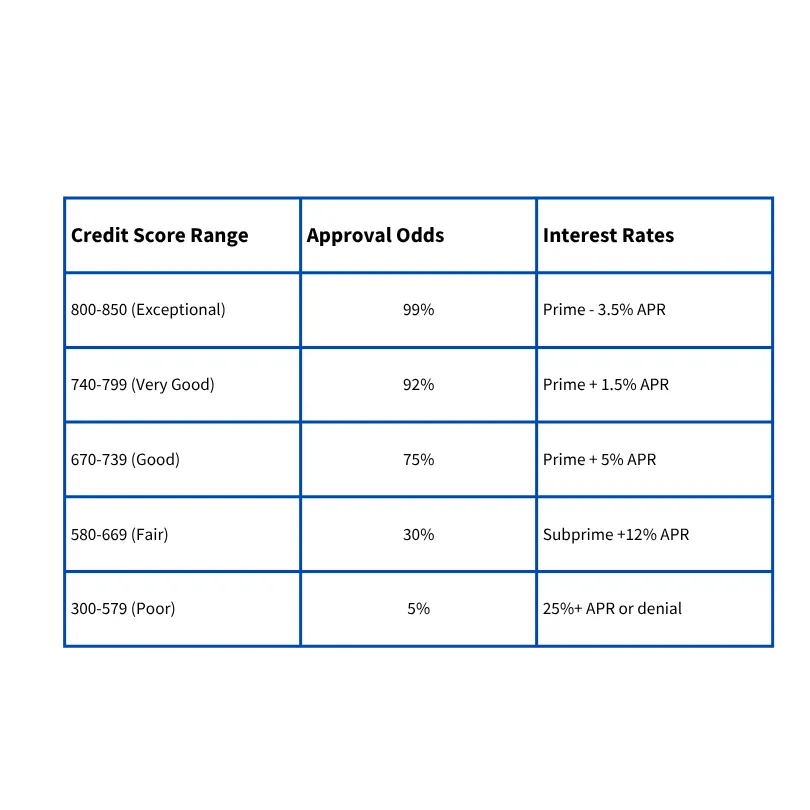

How Creditors Make Decisions

When you apply for a loan or card, lenders userisk-based pricing:

Types of Credit Accounts

1. Revolving Credit (Credit Cards)

Borrow up to a limit, repay flexibly

Pro Tip: Keeping balances below 8.9% of limits maximizes scores

2. Installment Loans (Auto/Mortgage/Student)

Fixed payments over set terms

Critical Note: Paying off early can temporarily lower scores by reducing credit mix

3. Open Credit (Utilities/Cell Phones)

Not always reported—but delinquencies hurt

Strategy: Request good payment history be added

4. Collection Accounts

Reported after 180 days of non-payment

Game Changer: Under FDCPA §809, collectors must prove the debt is yours

Know Your Credit Rights!

The FCRA is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application.You have the right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.You have the right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes. Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.You have the right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.You have a right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.The ECOA prohibits credit discrimination on the basis of sex, race, marital status, religion, national origin, age, or receipt of public assistance. Creditors may ask for this information (except religion) in certain situations, but may not use it to discriminate when deciding whether to grant you credit.

The ECOA protects consumers who deal with companies that regularly extend credit, including banks, small loan and finance companies, retail and department stores, credit card companies, and credit unions. Everyone who participates in the decision to grant credit, including real estate brokers who arrange financing, must follow this law. Businesses applying for credit also are protected by this law.The ECOA prohibits credit discrimination on the basis of sex, race, marital status, religion, national origin, age, or receipt of public assistance. Creditors may ask for this information (except religion) in certain situations, but may not use it to discriminate when deciding whether to grant you credit.

The ECOA protects consumers who deal with companies that regularly extend credit, including banks, small loan and finance companies, retail and department stores, credit card companies, and credit unions. Everyone who participates in the decision to grant credit, including real estate brokers who arrange financing, must follow this law. Businesses applying for credit also are protected by this law. You cannot be denied credit based on your race, sex, marital status, religion, age, national origin, or receipt of public assistance.

You have the right to have reliable public assistance considered in the same manner as other income. If you are denied credit, you have a legal right to know why. FACTA (Fair and Accurate Credit Transactions Act) is an amendment to FCRA (Fair Credit Reporting Act) that was added, primarily, to protect consumers from identity theft.

Know Your Credit Rights!

The FCRA is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application.You have the right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.You have the right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes. Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.You have the right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.You have a right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.The ECOA prohibits credit discrimination on the basis of sex, race, marital status, religion, national origin, age, or receipt of public assistance. Creditors may ask for this information (except religion) in certain situations, but may not use it to discriminate when deciding whether to grant you credit.

The ECOA protects consumers who deal with companies that regularly extend credit, including banks, small loan and finance companies, retail and department stores, credit card companies, and credit unions. Everyone who participates in the decision to grant credit, including real estate brokers who arrange financing, must follow this law. Businesses applying for credit also are protected by this law.The ECOA prohibits credit discrimination on the basis of sex, race, marital status, religion, national origin, age, or receipt of public assistance. Creditors may ask for this information (except religion) in certain situations, but may not use it to discriminate when deciding whether to grant you credit.

The ECOA protects consumers who deal with companies that regularly extend credit, including banks, small loan and finance companies, retail and department stores, credit card companies, and credit unions. Everyone who participates in the decision to grant credit, including real estate brokers who arrange financing, must follow this law. Businesses applying for credit also are protected by this law. You cannot be denied credit based on your race, sex, marital status, religion, age, national origin, or receipt of public assistance.

You have the right to have reliable public assistance considered in the same manner as other income. If you are denied credit, you have a legal right to know why. FACTA (Fair and Accurate Credit Transactions Act) is an amendment to FCRA (Fair Credit Reporting Act) that was added, primarily, to protect consumers from identity theft.

© 2024 @ Apollo Credit Processing LLC - All Rights Reserved

DUNS #:108691532